Toll Free: 1-888-928-9744

Toll Free: 1-888-928-9744

Published: Oct, 2015 | Pages:

105 | Publisher: Radiant Insights Inc.

Industry: Plastics | Report Format: Electronic (PDF)

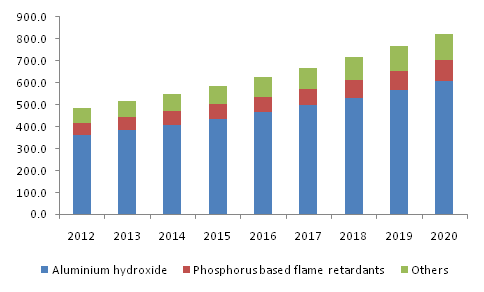

The Report Contains Non Halogenated Flame Retardants Market Size By Application (Polyolefins, Epoxy Resin, UPE, PVC, ETP, Rubber, Styrenics), By End Use Industry (Electrical, Construction, Transportation), By Product (Aluminum Hydroxide, Phosphorous Based), Competitive Analysis & Forecast, 2012 - 2020 Industry Overview Global non halogenated flame retardants market size is anticipated to reach 2.01 million tons by 2020, growing at CAGR of 7.3% from 2014 to 2020. Associated factors such as low heat and smoke emission are anticipated to drive non halogenated flame retardant market growth. Increase in safety materials demand in construction industry coupled with growth in infrastructure spending in emerging economies of Brazil, India, China and Russia is anticipated to drive the demand for construction industry. The Chinese construction industry recorded a double digit growth from 2008 to 2012. In 2013 the industry was valued at USD 1.78 trillion. China’s demand for non halogenated flame retardants is high due to the fact that the country has high production capacities of end-use industries. Shift towards replacing steel with plastics in the automotive industry in order to improve fuel efficiency by reducing the overall weight of the automobile is anticipated to drive non halogenated flame retardants market. The global demand for polymers from transportation industry was recorded as 20.00 million tons in 2006 and 24.92 million tons in 2011. A 10% reduction in weight results in about 5% to 7% fuel saving in an automobile. In addition, the reduced weight also helps control the emission of CO2 over the life cycle of the vehicle. Reduction in weight helps the overall performance of the vehicle in terms of its acceleration and handling. Stringent norms by regulatory bodies such as Europe, REACH & WEEE in European Union, EPA and Canadian Environmental Protection Act (CEPA), against use of flame retardants causing adverse environmental effects, are likely to favor non halogenated flame retardants market growth. They have some operational disadvantages such as color impartment and high loading level when compared with halogen based flame retardants which may hold back industry growth. These retardants can be added with nanoclays which may help in overcoming the drawbacks.North America non halogenated flame retardants market, by product, 2012-2020 (Kilo Tons)Product Overview Aluminium hydroxide was the largest product segment with valuation of over USD 350 million in 2013. Increasing concern for material health and safety in several industries specifically in the key economies of U.S. and Western Europe coupled with low cost advantages for aluminum hydroxide flame retardants manufacturers is anticipated to drive industry growth. Phosphorous based flame retardants were the second largest and accounted for over 10% of the total consumption in 2013 and are anticipated to witness higher gains of over 8% up to 2020. Inorganic and organic phosphorous flame retardants are two forms associated with this particular product. Increasing application scope coupled with technological advancements is likely to drive demand. End Use Overview Construction industry was the dominant end-use segment with a revenue generation exceeding USD 500 million in 2013. Increasing regulations for HSE in construction industries by REACH, EPA and other regulatory agencies has created new opportunities for industry growth for the forecast period. Transportation accounted for more than 20% of the total demand in 2013 and is anticipated receive moderate gains with an estimated CAGR of over 6.5% up to 2020. Growing fire safety regulations in transpirations industry are anticipated to drive the demand. Electrical end-use segment is anticipated to be the fastest growing with an estimated CAGR of over 7.5% from 2014 to 2020. Rise in demand for safety materials for pipe and wires used in electrical industry coupled with increasing electricity infrastructure in BRICS nations is anticipated to drive market growth. Regional Overview North America was the leading region with revenue exceeding USD 550 million in 2013. Growing expenditures on safety materials coupled with growth of major end-use industries in countries such as U.S. and Canada is anticipated to boost non halogenated flame retardant market. Europe accounted for over 30% of the demand and is anticipated to witness moderate growth rates up to 2020. Stringent rules have been implemented on imports and production of end-use products that are composed of toxic flame retardants. This factor is likely to be favorable for Europe demand development. Asia Pacific non halogenated flame retardants market is anticipated to be the fastest growing region over the forecast period, at an estimated CAGR at over 7.5% from 2014 to 2020. Presence of large scale manufacturing bases coupled with increasing construction spending particularly in China, India and Indonesia is anticipated to drive regional demand. Competitive Market Share The global non halogenated flame retardants market share is moderately fragmented. Albemarle dominated the market and accounted for over 13% share in 2013. Albemarle is engaged in manufacturing of these products for electrical equipments, textiles and transport vehicles. Key manufacturers include Clariant International Ltd, Chemtura, Italmatch Chemicals and BASF. Other prominent manufacturers include Thor Group Ltd, DSM, Lanxess Ltd, FRX Polymers, DuPont, Delamin, Huber Engineered Materials and Nabaltec AG.

Table of Content Chapter 1 Executive Summary Chapter 2 Non Halogenated Flame Retardants Industry Overview 2.1 Market segmentation 2.1.1 Global flame retardants market volume share by product, 2013 2.2 Market Size and Growth Prospects 2.3 Non Halogenated Flame Retardants - Value Chain Analysis 2.4 Non Halogenated Flame Retardants – Market dynamics 2.4.1 Market driver analysis 2.4.1.1 Regulatory support 2.4.1.2 Growing demand for plastics/polymers from transportation industry 2.4.1.3 Growing construction and infrastructure spending 2.4.2 Market restraint analysis 2.4.2.1 Lack of performance against halogenated flame retardants 2.5 Key opportunities - Prioritized 2.5.1 Key market opportunities 2.5.1.1 Adoption of nanotechnology for product development 2.5.1.2 Increasing market penetration in electricals industry particularly in Asia Pacific 2.6 Industry Analysis – Porter’s 2.7 Non Halogenated Flame Retardants – Company market share analysis, 2013 2.8 Non Halogenated Flame Retardants – PESTEL Analysis Chapter 3 Non Halogenated Flame Retardants Product Overview 3.1 Non halogenated flame retardants market volume share by product, 2013 & 2020 3.2 Aluminum Hydroxide 3.2.1 Global aluminium hydroxide flame retardants market volume and revenue, 2012-2020 3.2.2 Global aluminum hydroxide flame retardant market volume and revenue by region, 2012-2020 3.3 Phosphorous Based Flame Retardants 3.3.1 Global phosphorous based flame retardants market volume and revenue, 2012-2020 3.3.2 Global phosphorous based flame retardants market volume and revenue by region, 2012-2020 3.4 Others 3.4.1 Global other flame retardants market volume and revenue, 2012-2020 3.4.2 Global other flame retardants market volume and revenue by region, 2012-2020 Chapter 4 Non Halogenated Flame Retardants Application Overview 4.1 Non halogenated flame retardants market volume share by application, 2013 & 2020 4.2 Polyolefins 4.2.1 Global demand for non halogenated flame retardants from polyolefins, 2012-2020 (Kilo Tons) (USD Million) 4.3 Epoxy Resins 4.3.1 Global demand for non halogenated flame retardants from epoxy resins, 2012-2020 (Kilo Tons) (USD Million) 4.4 Unsaturated polyester (UPE) 4.4.1 Global demand for non halogenated flame retardants from UPE, 2012-2020 (Kilo Tons) (USD Million) 4.5 Polyvinyl chloride (PVC) 4.5.1 Global demand for non halogenated flame retardants from PVC, 2012-2020 (Kilo Tons) (USD Million) 4.6 Engineering thermoplastics (ETP) 4.6.1 Global demand for non halogenated flame retardants from ETP, 2012-2020 (Kilo Tons) (USD Million) 4.7 Rubber 4.7.1 Global demand for non halogenated flame retardants from rubber, 2012-2020 4.8 Styrenics (Kilo Tons) (USD Million) 4.8.1 Global demand for non halogenated flame retardants from styrenics, 2012-2020 (Kilo Tons) (USD Million) 4.9 Other 4.9.1 Global demand for non halogenated flame retardants from other applications, 2012-2020 (Kilo Tons) (USD Million) Chapter 5 Non Halogenated Flame Retardants End-Use Industry Overview 5.1 Global non halogenated flame retardant market volume share by end-use industry, 2013 & 2020 5.2 Electrical 5.2.1 Global demand of non halogenated flame retardants from electrical industry, 2012-2020 (Kilo Tons) (USD Million) 5.2.2 Global demand of non halogenated flame retardants from electrical industry volume and revenue by region, 2012-2020 (Kilo Tons) (USD Million) 5.3 Construction 5.3.1 Global demand of non halogenated flame retardants from construction, 2012-2020 (Kilo Tons) (USD Million) 5.3.2 Global demand of non halogenated flame retardants from construction, volume and revenue by region, 2012-2020 (Kilo Tons) (USD Million) 5.4 Transportation 5.4.1 Global demand of non halogenated flame retardants from transportation industry, 2012-2020 (Kilo Tons) (USD Million) 5.4.2 Global demand of non halogenated flame retardants from transportation, volume and revenue by region, 2012-2020 (Kilo Tons) (USD Million) 5.5 Others 5.5.1 Global demand of non halogenated flame retardants from other industries, 2012-2020 (Kilo Tons) (USD Million) 5.5.2 Global demand of non halogenated flame retardants from other industries volume and revenue by region, 2012-2020 (Kilo Tons) (USD Million) Chapter 6 Non Halogenated Flame Retardants Regional Overview 6.1 Non halogenated flame retardants market volume share by region, 2013 & 2020 6.2 North America 6.2.1 Market estimates and forecast, 2012-2020 (Kilo Tons) (USD Million) 6.2.2 Market estimates and forecast by product, 2012-2020 (Kilo Tons) (USD Million) 6.2.3 Market estimates and forecast t by end-use industry, 2012 to 2020 (Kilo Tons) (USD Million) 6.3 Europe 6.3.1 Market estimates and forecast, 2012-2020 (Kilo Tons) (USD Million) 6.3.2 Market estimates and forecast market by product, 2012-2020 (Kilo Tons) (USD Million) 6.3.3 E Market estimates and forecast by end-use industry, 2012-2020 (Kilo Tons) (USD Million) 6.4 Asia Pacific 6.4.1 Market estimates and forecast, 2012-2020 (Kilo Tons) (USD Million) 6.4.2 Market estimates and forecast by product, 2012-2020 (Kilo Tons) (USD Million) 6.4.3 Market estimates and forecast by end-use industry, 2012-2020 (Kilo Tons) (USD Million) 6.5 RoW 6.5.1 Market estimates and forecast, 2012-2020 (Kilo Tons) (USD Million) 6.5.2 Market estimates and forecast by product, 2012-2020 (Kilo Tons) (USD Million) 6.5.3 Market estimates and forecast by end-use industry, 2012-2020 (Kilo Tons) (USD Million) Chapter 7 Competitive Landscape 7.1 Albemarle Corporation 7.1.1 Company Overview 7.1.2 Financial Performance 7.1.3 Product Benchmarking 7.1.4 Strategic Initiatives 7.2 Israel Chemicals Ltd. 7.2.1 Company Overview 7.2.2 Financial Performance 7.2.3 Product Benchmarking 7.2.4 Strategic Initiatives 7.3 Chemtura Corporation 7.3.1 Company Overview 7.3.2 Financial Performance 7.3.3 Product Benchmarking 7.3.4 Strategic Initiatives 7.4 Clariant International Ltd. 7.4.1 Company Overview 7.4.2 Financial Performance 7.4.3 Product Benchmarking 7.4.4 Strategic Initiatives 7.5 Italmatch Chemicals 7.5.1 Company Overview 7.5.2 Financial Performance 7.5.3 Product Benchmarking 7.5.4 Strategic Initiatives 7.6 Huber Engineered Materials 7.6.1 Company Overview 7.6.2 Financial Performance 7.6.3 Product Benchmarking 7.6.4 Strategic Initiatives 7.7 BASF S.E. 7.7.1 Company Overview 7.7.2 Financial Performance 7.7.3 Product Benchmarking 7.7.4 Strategic Initiatives 7.8 Thor Group Ltd. 7.8.1 Company Overview 7.8.2 Financial Performance 7.8.3 Product Benchmarking 7.9 Lanxess A.G. 7.9.1 Company Overview 7.9.2 Financial Performance 7.9.3 Product Benchmarking 7.9.4 Strategic Initiatives 7.10 DSM N.V. 7.10.1 Company Overview 7.10.2 Financial Performance 7.10.3 Product Benchmarking 7.10.4 Strategic Initiatives 7.11 FRX Polymers Inc. 7.11.1 Company Overview 7.11.2 Financial Performance 7.11.3 Product Benchmarking 7.11.4 Strategic Initiatives 7.12 Nabaltec A.G. 7.12.1 Company Overview 7.12.2 Financial Performance 7.12.3 Product Benchmarking 7.12.4 Strategic Initiatives 7.13 Delamin Ltd. 7.13.1 Company Overview 7.13.2 Financial Performance 7.13.3 Product Benchmarking 7.13.4 Strategic Initiatives 7.14 DuPont 7.14.1 Company Overview 7.14.2 Financial Performance 7.14.3 Product Benchmarking 7.14.4 Strategic Initiatives Chapter 8 Methodology & Scope 8.1 Research Methodology 8.2 Research Scope & Assumptions 8.3 List of Data Sources

List of Table TABLE 1 Non Halogenated Flame Retardants – Industry Summary & Critical Success Factors (CSFs) TABLE 2 Global non halogenated flame retardants market volume & revenue, 2012 – 2020 (Kilo Tons), (USD Million) TABLE 3 Global non halogenated flame retardants market volume by region, (Kilo Tons), 2012 - 2020 TABLE 4 Global non halogenated flame retardants market revenue by region, (USD Million), 2012 – 2020 TABLE 5 Global non halogenated flame retardants market volume by product, (Kilo Tons), 2012 - 2020 TABLE 6 Global non halogenated flame retardants market revenue by product, (USD Million), 2012 – 2020 TABLE 7 Global non halogenated flame retardants market volume by application, (Kilo Tons), 2012 - 2020 TABLE 8 Global non halogenated flame retardants market revenue by application, (USD Million), 2012 - 2020 TABLE 9 Global non halogenated flame retardants market volume by end-use, (Kilo Tons), 2012 – 2020 TABLE 10 Global non halogenated flame retardants market revenue by end-use, (USD Million), 2012 – 2020 TABLE 11 Non halogenated flame retardants – Key market driver analysis TABLE 12 Basic requirements of automotive materials TABLE 13 Non Halogenated Flame Retardants – Key market restraint analysis TABLE 14 Halogenated flame retardants versus non halogenated flame retardants TABLE 15 Global aluminum hydroxide flame retardants market volume and revenue, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 16 Global aluminum hydroxide flame retardant market volume by region, 2012 – 2020 (Kilo Tons) TABLE 17 Global aluminum hydroxide flame retardant market revenue by region, 2012 – 2020 (USD million) TABLE 18 Global phosphorous based flame retardants market volume and revenue, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 19 Global phosphorous based flame retardants market volume by region, 2012 – 2020 (Kilo Tons) TABLE 20 Global phosphorous based flame retardants market revenue by region, 2012 – 2020 (USD million) TABLE 21 Global other flame retardants market volume and revenue, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 22 Global other flame retardants market volume by region, 2012 – 2020 (Kilo Tons) TABLE 23 Global other flame retardants market revenue by region, 2012 – 2020 (USD million) TABLE 24 Global demand for non halogenated flame retardants from polyolefins, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 25 Global demand for non halogenated flame retardants from epoxy resins, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 26 Global demand for non halogenated flame retardants from UPE, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 27 Global demand for non halogenated flame retardants from PVC, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 28 Global demand for non halogenated flame retardants from ETP, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 29 Global demand for non halogenated flame retardants from rubber, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 30 Global demand for non halogenated flame retardants from styrenics, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 31 Global demand for non halogenated flame retardants from other applications, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 32 Global demand of non halogenated flame retardants from electrical industry volume and revenue, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 33 Global volume of non halogenated flame retardants from electrical industry by region, 2012 – 2020 (Kilo Tons) TABLE 34 Global revenue of non halogenated flame retardants from electrical industry by region, 2012 – 2020 (USD million) TABLE 35 Global demand of non halogenated flame retardants from construction, volume and revenue, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 36 Global volume of non halogenated flame retardants from construction by region, 2012 – 2020 (Kilo Tons) TABLE 37 Global revenue of non halogenated flame retardants from construction by region, 2012 – 2020 (USD million) TABLE 38 Global demand of non halogenated flame retardants from transportation, volume and revenue, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 39 Global volume of non halogenated flame retardants from transportation by region, 2012 – 2020 (Kilo Tons) TABLE 40 Global revenue of non halogenated flame retardants from transportation by region, 2012 – 2020 (USD million) TABLE 41 Global demand of non halogenated flame retardants from other industries volume and revenue, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 42 Global volume of non halogenated flame retardants from other industries by region, 2012 – 2020 (Kilo Tons) TABLE 43 Global revenue of non halogenated flame retardants from other industries by region, 2012 – 2020 (USD million) TABLE 44 North America non halogenated flame retardants market volume & revenue, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 45 North America non halogenated flame retardants market volume by product, 2012-2020 (Kilo Tons) TABLE 46 North America non halogenated flame retardants market revenue by product, 2012-2020 (USD million) TABLE 47 North America non halogenated flame retardants market volume by end-use industry, 2012-2020 (Kilo Tons) TABLE 48 North America non halogenated flame retardants market revenue by end use industry, 2012-2020 (USD million) TABLE 49 Europe non halogenated flame retardants market volume & revenue, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 50 Europe non halogenated flame retardants market volume by product, 2012-2020 (Kilo Tons) TABLE 51 Europe non halogenated flame retardants market revenue by product, 2012-2020 (USD million) TABLE 52 Europe non halogenated flame retardants market volume by end-use industry, 2012-2020 (Kilo Tons) TABLE 53 Europe non halogenated flame retardants market revenue by end use industry, 2012-2020 (USD million) TABLE 54 Asia Pacific non halogenated flame retardants market volume & revenue, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 55 Asia Pacific non halogenated flame retardants market volume by product, 2012-2020 (Kilo Tons) TABLE 56 Asia Pacific non halogenated flame retardants market revenue by product, 2012-2020 (USD million) TABLE 57 Asia Pacific non halogenated flame retardants market volume by end-use industry, 2012-2020 (Kilo Tons) TABLE 58 Asia Pacific non halogenated flame retardants market revenue by end use industry, 2012-2020 (USD million) TABLE 59 RoW non halogenated flame retardants market volume & revenue, 2012 – 2020, (Kilo Tons) (USD Million) TABLE 60 RoW non halogenated flame retardants market volume by product, 2012-2020 (Kilo Tons) TABLE 61 RoW non halogenated flame retardants market revenue by product, 2012-2020 (USD million) TABLE 62 RoW non halogenated flame retardants market volume by end-use industry, 2012-2020 (Kilo Tons) TABLE 63 RoW non halogenated flame retardants market revenue by end use industry, 2012-2020 (USD million)

Speak to the report author to design an exclusive study to serve your research needs.

Your personal and confidential information is safe and secure.